patrick.net

An Antidote to Corporate Media

1,193,707 comments by 13,881 users - AmericanKulak, Eric Holder, HeadSet, Onvacation online now

Home Prices are COLLAPSING again!!!!!!!!!

2010 Oct 24, 2:37pm 28,174 views 125 comments

« First « Previous Comments 15 - 54 of 125 Next » Last » Search these comments

We have:

1. "DECREASES in nominal household incomes. Fact."

Fiction currently. That's true for 2008 and 2009 when 13M jobs were shedded. 2010 is an increase in nominal wages. Per the census bureau stats, Average hourly earnings of all employees on private nonfarm payrolls increased by 1 cent to $22.67 in September. Over the past 12 months, average hourly earnings have increased by 1.7 percent.

2. "SIGNIFICANT DECREASES in genuine inflation-adjusted (incl. food/energy/insurance/medical insurance/tuition, etc.) household incomes. Fact."

True, but stocks are up nearly 80% off the March 2009 lows so people with inflation adjusted assets are doing fine so a certain amount of the household is doing fine.

3. "DECREASES in jobs. Fact."

2010 is net additions. Again double check your census data. http://www.bls.gov/news.release/pdf/empsit.pdf

4. "DECREASE in new household formation. Fact."

New household formation is delayed, the significance depends on whether you think this is temp or perm. If temp, it just means that household formation is higher prospectively.

5. "HUGE INCREASES in supply with new foreclosure records being hit every month or so."

Good reason why house prices are not going up but does not explain why it wil dip below March 2009. New homes and apartment are currently built at 1/3 to 1/4 of the levels in 2002-2006.

"Despite heaps of government gimmicks and giveaways combined with the lowest rates of interest, sales of existing and new homes are SIGNIFICANTLY BELOW EVEN LAST YEAR’S DUMP LEVELS AND HIT MULTI-DECADE LOWS this summer."

Last summer/fall was quite a bump up due to the tax credit so 2009 particularly was far from dump levels to comp with.

"Where are all of the billionaires from the UAE? Why aren’t they buying up all of our houses? Oh, that’s right - their bubble was even bigger than ours, and it completely burst as well. This real estate bubble is worldwide and is the largest speculative bubble ever manifested, all courtesy of sustained record-low interest rates in the developed world as their productive economies no longer exist and depend solely on bubbles to sustain themselves."

The effect of foreign buyer's are built over a period of time. In 2010, the % of US real estate under foreign ownership is higher than ever.

Oh please. In just a couple of months we’ve nearly wiped out the gains from the tax credit. We’ll soon pass the 2009 bottom, and all of a sudden he will be wrong and others will be right

I'm laughing. You forgot to add "I think" before that sentence. Unless you have a crystal ball in your house that I don't know about...

It’s calling someone out for their baseless claims when the data slowly trickles in to show they were wrong

Once again. He's NOT wrong. (yet) Maybe he will be, maybe he won't be. But Jesus Christ. You are the epitome of arrogance to call someone out because you THINK they will be shown wrong in the future.

It’s already started double-dipping.

OK Mr. show me the data. Please, show me why you think that the economy is already double dipping.

I’m laughing. You forgot to add “I think†before that sentence.

No, I forgot to add "from Clear Capital's housing index which showed a two-month drop of 6%". Whether it happens over 3, 6 or 9 months is irrelevant. What is relevant is that you are intentionally ignoring market trends that many of us have been expecting and are coming true. Price increases when the credit was introduced didn't surprise me one single bit. Nor does this data.

Once again. He’s NOT wrong. (yet)

Tell him that then. He admitted above that he was wrong about the tax credit. He's gone from a position of "it had nothing to do with price increases" (in which case then, what did?) to saying that it had some impact, but less than we think. In a few months, he'll be like "okay I was totally wrong". Which is fine, I don't care about people being wrong. I just point out that if their predictions are based on nothing more than an arbitrary guess, their future arbitrary guesses will be rightly derided. Again, the issue is not what he claims, but WHY he makes the claims.

Maybe he will be, maybe he won’t be. But Jesus Christ. You are the epitome of arrogance to call someone out because you THINK they will be shown wrong in the future.

No, the data is now backing up the notion that he is wrong, and he admits it. Now stop kissing up to him, he's a few steps closer to reality than you are at this point.

No, the data is now backing up the notion that he is wrong, and he admits it. Now stop kissing up to him, he’s a few steps closer to reality than you are at this point.

Scroll half-way up the page. See that big-ass graphic. One, maybe two more months and we will be below 2009's low mark. You think it won't happen? Fine. I do. The fundamentals of the market do not support these prices and there was nothing pre-credit to indicate it was easing on its own. Hence, prices will continue falling.

SF Ace,

Household incomes ARE GOING DOWN. Nominal wages are meaningless - the "gain" for 2010 is microscopic and is a STEP BACK once genuine inflation statistics are used. I never mentioned WAGES - you just brought it up out of nowhere.

Most people still have a LOSS in their 401K from 2007 yet prices of food, tuition, medical insurance, etc. HAVE GONE UP. Assets have GONE DOWN, but costs have GONE UP.

We've lost millions upon millions of jobs since the bust began. 2010's numbers (which are PATHETIC given trillions of dollars of stimulus/debt) are going to be revised significantly DOWNWARD by the BLS. This was in the September BLS report.

New household formation is particularly ugly, especially considering the amount of debt new college graduates are taking on while belonging to a cohort with an extremely high UE rate.

I can't take it anymore

klarek says

I might be arrogant or rude

You are an arrogantly rude uppity chicken little. You are also certainly far from helpful. You also believe that DC is immune because it is something special. You don't have your head in the sand, it is firmly implanted up your ass.

I just demand a more sophisticated explanation other than “that was the bottomâ€, or in your case “since we haven’t crossed it yet, he must be rightâ€.

You have provided some sophisticated analysis as to why it wasn't the bottom? I don't know if it was the bottom or not. There will be a bottom somewhere (if we haven't hit it already), however, and I'm missing your sophisticated analysis as to when it will be. Oh wait a minute, we have had the bottom - only in DC, though. How sophisticated.

It’s already started double-dipping.

How do you arrive at this conclusion? Oh, with your sophisticated analysis:

I think that upon the credit’s inception, we were nationally about 10-15% overpriced and will very soon be at that same level again. I think this winter will be very brutal, prices will continue to tank, and *maybe* we will see a temporary period in the spring where they level off a little bit, if they’ve fallen enough to feel the spring summer “bump†they normally do.

Where did you get this? Is this not your opinion - given in the same manner which you evidently despise? Where are the facts to back up the "10-15% overpriced" - and are we going to be at the 10-15% overpriced level or back to where we should be? Or is this only in DC? What is your point anyway?

The fundamentals of the market do not support these prices and there was nothing pre-credit to indicate it was easing on its own. Hence, prices will continue falling.

What are these fundamentals?

I'm done. I rescind my nomination of PolishKnight as the idiot of the year - I have discovered a new contender.

Scroll half-way up the page. See that big-ass graphic. One, maybe two more months and we will be below 2009’s low mark

Oh, is that how it works? If the line points down, it will continue to point down? Didn't know that. So, prices will continue to fall forever then?

I just point out that if their predictions are based on nothing more than an arbitrary guess, their future arbitrary guesses will be rightly derided. Again, the issue is not what he claims, but WHY he makes the claims.

His predictions are his best guess, just as yours are. Predictions by their very nature are someone's best guess.

Again--you can disagree with him if you like, but don't call him wrong. Because he's not. It's not a foregone conclusion that prices will continue to drop or that they will establish a new low. They might. They might not.

You also believe that DC is immune because it is something special.

No I did not say it's special. Trust me, I've heard that b.s. around here for the past four years while watching the market tank. I do however know how to look at local GDP trends and compare them to national, and how to extrapolate our pre-bubble market onto what we would have had the bubble never existed. Sorry if that is too complicated, pea-brain, but it does NOT mean this area is special. It means the fundamentals support a certain pricing level, and some areas correct at a different extent than others do.

Where did you get this? Is this not your opinion - given in the same manner which you evidently despise? Where are the facts to back up the “10-15% overpriced†- and are we going to be at the 10-15% overpriced level or back to where we should be? Or is this only in DC? What is your point anyway?

I was referring to the national level. In my area, probably a bit less, though certain pockets around here that have only fallen ~15% so far are destined (by my calculations) to drop another 30%. Due to a lack of foreclosures in those areas, the correction may occur over a very long period of time, scaled out by inflation.

The data is largely from Case-Shiller. Go look it up yourself, I'm not your fucking tutor.

What are these fundamentals?

I have said it many times in other threads: INCOME. Specifically, household GDP. That is the most important. Others would be loan durations, interest rates, govt incentives (tax breaks), supply/demand (which largely respond to the market and don't significantly alter the equilibrium), tiered wage growth, savings rates (and propensity to consume versus save), etc.

Just by asking what these fundamentals are, I can tell you didn't know this. So maybe next time you are actually curious and want me to explain it to you in a way that isn't rude, you don't shoot the question at me like a complete fucking prick yourself. OK?

His predictions are his best guess, just as yours are. Predictions by their very nature are someone’s best guess.

No, his predictions are both baseless and ever-changing.

Again–you can disagree with him if you like, but don’t call him wrong. Because he’s not. It’s not a foregone conclusion that prices will continue to drop or that they will establish a new low. They might. They might not.

I understand philosophically the argument that because it hasn't happened yet, etc. But the data right now is contradicting him, and he is the one admitting he is wrong. The timing of the price increases with the credit's introduction to the market is no coincidence. Logically, whatever it created (the gain since spring 2009) will not continue to exist. It can't. Just like the housing bubble and all the delusional folks back in 2006-7 insisting that the market had bottomed, things were turning around, etc. There is an inevitability in all of this and unless there is an actual mathematical or statistical basis for someone's arguments, they do not hold equal footing with contrary, numerically-based opinions.

Again, the disagreement is not simply about his position, it's about his methodology (or lack of one). I try to second-guess my opinions all the time, but the numbers simply do not support a significant change of mind on the matter.

Just by asking what these fundamentals are, I can tell you didn’t know this. So maybe next time you are actually curious and want me to explain it to you in a way that isn’t rude, you don’t shoot the question at me like a complete fucking prick yourself. OK?

I'm not curious as to what you think. I'm curious as to how you can walk through the front door with such a large head.

If you don't want to be treated like a "complete f'ing prick", stop acting like one.

Scroll half-way up the page. See that big-ass graphic. One, maybe two more months and we will be below 2009’s low mark

Oh, is that how it works? If the line points down, it will continue to point down? Didn’t know that. So, prices will continue to fall forever then?

Har har, smartass. There was nothing prior to the tax credit that indicated the market was going to rebound.

Har har, smartass. There was nothing prior to the tax credit that indicated the market was going to rebound.

If you look at the august pending sales index in the west, it is 101.1 in August 2010. vs. 100.4 in March and 107.9 in April. In other words, the effect of the tax credit expiration is already gone by fall as the August pending will convert into sales by around October. If the pending home sales trend continue into September (which is likely based on mortgage application indicator for purchases which have been rising), we will see the same type of sales in May, June for homes sales this fall, which would not lead to double dip prices. At best it would approach the March 2009 low.

Here's some evidence that seems to contradict your foregone conclusion theory... It's why I'm not convinced we're in for another large drop in prices.

If you don’t want to be treated like a “complete f’ing prickâ€, stop acting like one.

I had nothing bad to say to you until you approached me like an asshole. My tone to other people isn't always nice, but I get frustrated with bullshitters. If you don't like that, then either ignore it and talk to me like a normal person or don't talk to me at all.

I’m not curious as to what you think.

Oh really?

-You have provided some sophisticated analysis as to why it wasn’t the bottom?

-How do you arrive at this conclusion?

-Where did you get this? Is this not your opinion - given in the same manner which you evidently despise?

-Where are the facts to back up the “10-15% overpriced†- and are we going to be at the 10-15% overpriced level or back to where we should be? Or is this only in DC?

-What is your point anyway?

-What are these fundamentals?

Yes, you were curious. And thankless.

Here’s some evidence that seems to contradict your foregone conclusion theory… It’s why I’m not convinced we’re in for another large drop in prices.

And it was a good anecdotal case.... for a particular market. From NAR. I do not ignore points like that, but they aren't exactly overwhelming evidence that the market is near bottom. Give it a few more months of Case Shiller reports without govt interference (and, let's not forget, with rates this low prices SHOULD be increasing on their own), and see what happens. The writing is already on the wall.

I had nothing bad to say to you until you approached me like an asshole. My tone to other people isn’t always nice, but I get frustrated with bullshitters. If you don’t like that, then either ignore it and talk to me like a normal person or don’t talk to me at all.

I'm frustrated with bullshitters, too.

Yes, you were curious. And thankless.

I'm thankful I remembered the ignore feature. Good bye.

How do fundamentals, past data, theroy, graphs, charts and history help forcast this pozi market built on fraud.

everyone here still speak as if this is a free housing market/ economy that adhears to the natural forces of supply and demand.

How does one plug fraud into a forcast for the future?

I’m thankful I remembered the ignore feature. Good bye.

Door, ass, way out, don't hit, etc.

How does one plug fraud into a forcast for the future?

Ignore the fraud. Focus on the moving parts that are real. When there are no more left and it all becomes fraud, buy shotgun and eat soylent green.

Give it a few more months of Case Shiller reports without govt interference (and, let’s not forget, with rates this low prices SHOULD be increasing on their own), and see what happens. The writing is already on the wall.

Fair enough. The writing on my wall just says something different I guess.

I never for one second back in 2007 considered the possibility that the government would not intervene. Anyone betting on that assumption was making a big mistake.

Sorry, but nobody anticipated the degree to which the government would intervene, including experts like Meredith Whitney who've admitted as much.

Sorry, but nobody anticipated the degree to which the government would intervene, including experts like Meredith Whitney who’ve admitted as much.

Exactly. My assumption was that the free-market (Republicans) in Congress and/or the same in the White House (Bush) would let the free market rule, since that has always been their stated principle (hah).

Instead what we got was the Fed buying multiple triliions - TRILLIONS - worth of crap mortgage bonds at crazy over-valuations and thereby forcing effective mortgage rates down to near unprecedented levels around 4.5%. Plus various incentives, such as the $8k tax break, to get the suckers back into the game.

This massive socialization of the losses stopped the free-fall in the prices, but as we see, there is still downward momentum in the market.

The Case-Shiller index for July-Aug-Sep should be out later this week. Calculated Risk predicted it would likely show dropping prices again, even though there would be a small tail of the tax-credit-induced transactions in the data. We shall soon see.

Correction: It is the June-July-August data that is out today. Someone will surely start a thread on this topic.

wait wait wait one second …. I know that one of you kept telling me that the homebuyer credit was not making any difference. Whats up with that?

Dude, when prices go up, it is not because of homebuyer credit. When they fall, though, it is because the homebuyer credit went away. House prices must always go up, the bottom must always be in the past. It is always a great time to buy whatever the nice salesman is selling.

Stop keeping notes and asking so many questions. Sheesh...

I know it's just anecdotal, but I am definitely seeing the higher end homes in my working class area of the Bay Area (those in the 350-450k range) sitting a lot longer, and go pending only to end up active again.

The home we were considering making an offer on I was sure would have an offer right away, it's a nice home on a nice lot and is in move in condition, and is priced at it's 1999 asking price. The first weekend open house had a few lookers there, we went back to look at the house again at last weekends open house and it was empty.

The upper end in my area is now close price wise to the lower end of Lamorinda and the WC/Pleasant Hill prices. There was a serious disconnect for a while between the lower end (which was/is back to pre-2000) and the mid-higher end that was maintaining 2002-2004+ prices. I see that dynamic starting to crack.

Everyone has to live somewhere. The houses will be still occupied either by owners or renters. There will be always homeowners that need to move because of the family circumstances (new job, marriage, divorce, etc.). If they can not move because they can not sell, then the obvious solution is to find someone to trade the house with.

E.g. I found a job in Georgia but can not sell my house in Tennessee: let's find someone who wants to move from Georgia to Tennessee and buy each others houses. It is called permanent house swap. Tell me what is wrong with this type of transaction.

If one googles "permanent house swap" a bunch of sites comes up where creative homeowners happily trade their houses. - thousands of postings!!! The falling prices affect them much less than those just sitting in a house that does not sell trying to get last year's price.

That’s my argument all along. How can a person afford to pay 5-6 times his/her gross income towards the mortgage. It is way out of whack if you compare it to historic norm of 3 times the income.

Now that we had prices 5-6 times incomes for the past 10 years or so, the higher multiple is still being marketed by realtors as the new normal. I find it troubling, to find people who only came to Bay Area over the past 10 years unable to relate to what "normal is" prior to the bubble and decades before the year 2000.

to find people who only came to Bay Area over the past 10 years unable to relate to what “normal is†prior to the bubble and decades before the year 2000

4% interest rates go a long way towards softening the blow.

Just wait for 3.

I don’t see why we have to have inflation in all markets at the same time.

that will only happen if the general wage level increases, and that can only happen when unemployment goes away.

High gold prices are great if you are gold miner or own a gold mine. Same thing with all other producer price rises.

In a service economy, however, the vast majority of people are out in woo-woo land WRT wealth creation. Granted, if you sell something the gold producers want, you will do well, and there is some follow-on effects there, but overall I just see retrenchment, and since real estate is most everyone's #1 expense and has a production cost of approximately $0, it is the sector that can serve as a shock absorber best.

But I could be wrong. I've noticed out here a couple of operators have bought up all the multifamily housing. Location monopoly right out of Monopoly®, LOL.

Why it have to be so complicated? General rule of thumb is when inflation picks up, so does income and wages to catch up. That has been the case in India and China. Not sure of China but I can say for sure of India. Incomes have skyrocketed to match the booming real estate and other cost of living.

Just by asking what these fundamentals are, I can tell you didn’t know this. So maybe next time you are actually curious and want me to explain it to you in a way that isn’t rude, you don’t shoot the question at me like a complete fucking prick yourself. OK?

I’m not curious as to what you think. I’m curious as to how you can walk through the front door with such a large head.

If you don’t want to be treated like a “complete f’ing prickâ€, stop acting like one.

This is my first time here and I'm new to the US real estate market so I'm trying to learn what I can where I can. Klarek, I suspect that someone here has more than one account and is using different names to offer himself "public" support. I completely understand what you're saying. I've been looking to buy a house and in the last two weeks, about 75% of all the houses I've been looking at have had price reductions. Many are being re-posted under different MLS numbers. With millions more foreclosures in the works, and fewer and fewer people able to buy, I don't see how prices can go anywhere BUT down. I've decided to watch and wait for a while longer.

So the majority of US metro areas didn’t fall then, right?

Read between the lines. The article reports sales activity has dropped "25% from the previous year." That's a 25% drop from a BAD year. Without adequate sales activity, the excessive inventory cannot be removed from the market. Also, banks are withholding literally millions of REOs from the market so as not to swamp an already bloated market. Furthermore, every day that goes by, more properties are being added to the shadow inventory via foreclosures, adding further downward pressure in the future to prices once these properties are forced into the market.

Keep in mind also that this inventory is not being diminished with record low fixed rate mortgages. What happens when interest rates are eventually forced up?

Keep in mind also that this inventory is not being diminished with record low fixed rate mortgages. What happens when interest rates are eventually forced up?

If history is any guide, then prices will be rising...

If history is any guide, then prices will be rising…

Interest rates have historically been PUSHED up by the Fed, never forced up by the macro situation.

The current Ireland and Greece case is a bit different from Volcker in 1979.

If history is any guide, then prices will be rising…

Interest rates have historically been PUSHED up by the Fed, never forced up by the macro situation.

The current Ireland and Greece case is a bit different from Volcker in 1979.

http://research.stlouisfed.org/fred2/series/MORTG/

I agree--this time might be different. Just usually it isn't...

We’re not even halfway to terminal velocity.

Prepare for housing prices not seen since 1977.

Then total economic collapse.

Housing speculators will be burning their empty buildings, even with Section 8 tenants in them, to uncover earth they can use to plant potatoes.

The entire country has been deindustrialized and the high-paying craft work jobs are all in slave states like China. All of the displaced workers ended up in part time jobs at WalMart, on the streets, dead or in one way or another speculating in real estate. No one in their right mind will buy a building as an investment in the next three generations if civil societies don’t crumble and if the US doesn’t devolve into a feudal dystopia of disconnected warlord states.

The best we can hope for is a long-term economic collapse. The worst is collapse, followed by civil war and the rise of theocratic warlord states, led by Jesufascist end-timers.

Plant potatoes and teach wife and kids how to handle light and heavy ordnance.

Man, I've been missing a lot of fun since I bought my house in January.

I hate to break it to the DOOM soothsayers, but your stacking your chips to bet against the free world's most powerful government. QE2 is already inflating us out of our debt hole and re-engergizing the economy. You need to break away from the sheep and start running with the wolves.

We are at the cusp of America's largest economic boom in the history of human economic booms. Hold on tight because the BOOMers are here!

I agree–this time might be different. Just usually it isn’t…

Every time is different. The America of 1800, 1850, 1900, and 1950 was under-developed and needed more labor to get business rolling.

Today, not so much, and we have trained about two billion offshore people to do many of our wealth-creating jobs for $10/day, if that.

Income disparities are more like 1929 than 1949. Credit cannot bridge this gap permanently.

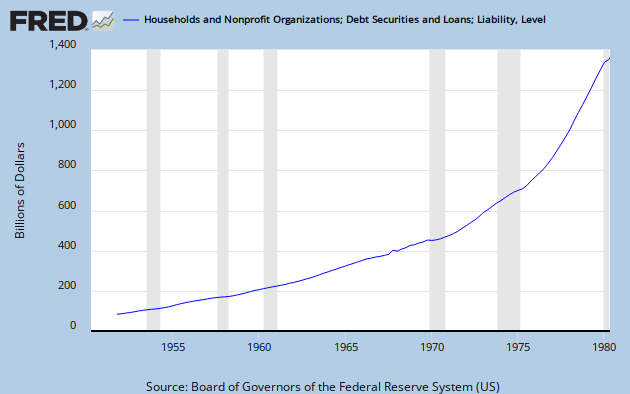

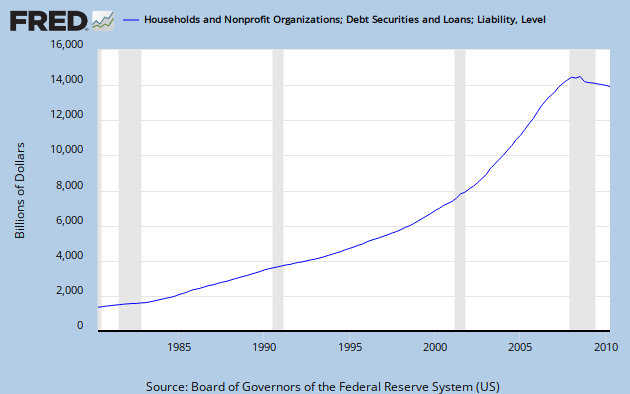

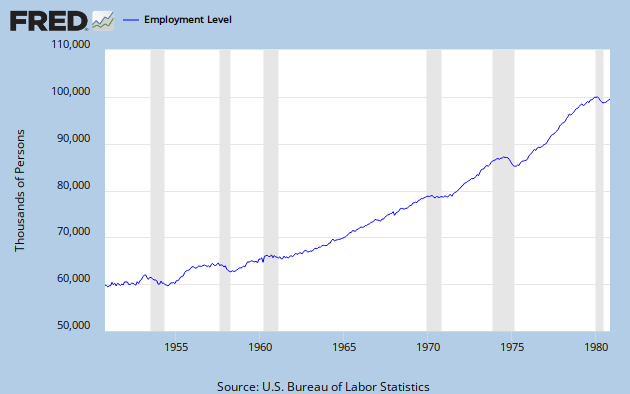

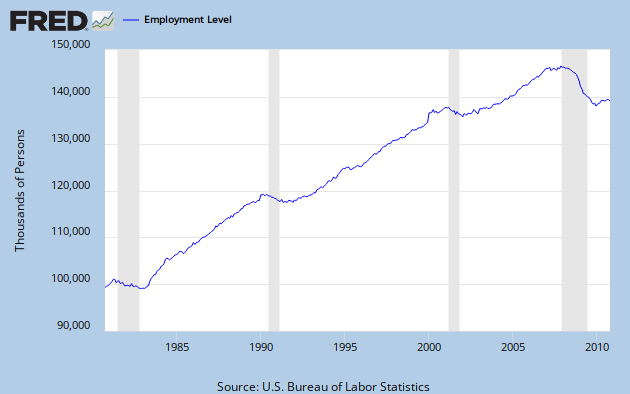

Hmm. Here's two charts:

{kind=link}

{kind=link}

While they look very similar, I think the underlying dynamics are very different. The bump in 1973-1979 may have been due to the baby boom -- and women -- entering the work force en masse. There was of course high inflation during this time, the minimum wage doubled from $1.60 to $3.35, 1970 to 1981.

Wages didn't double 2000-2010, that's for sure. Neither did employment.

{kind=link}

{kind=link}

yep, deficit spend and nationalize the debt to start off a boom!!!

its working so well in greece, ireland, iceland!!! what could go wrong?

You have it backwards. Greece, Ireland, Iceland did not nationalize debt before the collapse. They nationalized as a consquence.

Businesses do this all the time. Credit is used during the lean times to float until the flush times. Retailers don't even hit the black until Black Friday.

You can't throw your citizens overboard during the down business cycles (although the Tea Party is working as hard as hell to euthanize "worthless" people getting government help). They forget that these are the same people needed when the economy booms.

If we are worse of than Ireland, it is because of our endless wars of occupation in Iraq and Afghanistan.

Every time is different.

Yes and no. If you look hard enough you'll find differences. But I think some general trends stay remarkably similar.

« First « Previous Comments 15 - 54 of 125 Next » Last » Search these comments

5.9% drop in US home prices in two months!!!

http://www.clearcapital.com/company/pr_details.cfm?source=patrick.net&position=30686#header