patrick.net

An Antidote to Corporate Media

1,203,228 comments by 14,287 users - Ceffer, Onvacation, The_Deplorable online now

Secular deleveraging for the next decade or more ...

2012 Feb 17, 1:11am 12,243 views 36 comments

« First « Previous Comments 14 - 36 of 36 Search these comments

ust because you're either in the middle or working class doesn't mean you can't get a "piece of the action" because as we speak people are still making an awful lot of money. Today the DOW is up over 13,000 for the first time since 2008.

Well why do you think that is? Because the government is propping up the stock market just like they are trying to prop up all assets.

edvard2, my goal here is to understand what's going on and to analyze the magnitude of the risk. A major financial calamity doesn't just happen. It happens for a reason: because of malinvestment, because of bad bets, because of sovereign dysfunction, etc, etc, etc. So pretty much, what I want is to understand and get a clear picture of the problem.

What steps you choose to take is a matter of opinion. For example, guns and gold for doomsday believers. If you think bad inflation is coming, stocks are actually a good choice as we say hello to Dow 50,000. If you think deflation for now but things will recover without default or bad inflation, then government bonds are a great deal.

Anyways, forget discussing the solution. Analyzing the problem is a big enough task as it is. In fact, we don't exactly know how this debacle will unfold, so claiming one solution over another is like betting blindly. The only thing we know is that someone's gonna get hurt... real bad!

Speaking frankly, in the end what does any of this mean? Just because you're either in the middle or working class doesn't mean you can't get a "piece of the action" because as we speak people are still making an awful lot of money. Today the DOW is up over 13,000 for the first time since 2008. In fact the market has been doing pretty well for some time now. So is it better to sit around and worry about what might or might not happen? Is it worthwhile to constantly look at the numbers, the charts, and so on and guesstimate that the end is near and basically stay out of the market?

I say this as someone who for YEARS was also highly skeptical, but invested anyway for the hell of it.

Just remember that there are many, many people who are extremely intent on making money and most do so either directly or indirectly participating in the market.

Middle class suffer the worst taxation. They are between earned income and then get hit with AMT. They mostly get no capital gains or carried interest. The middle class is being screwed to the wall. To quote carlin, they do all of the work, pay all of the taxes.

In the old days, interest in passbook savings accounts was statutory 5.25% - this meant people could save for the future, beat inflation, and not have to risk anything to do so.

Now we have to risk everything just to beat inflation, which , by the way it was calculated in 1980 is 11% /year.

DOW 13000 doesn't mean my salary went up. It means food,gas rent went up, salaries were stagnant, and unless I gamble with the family food-gas-tuition-college-retirement money, I get screwed by both inflation and taxes.

You invested for the hell of it because you can tolerate a loss. Most people who lose stuff with families means moving back in with mom and dad and because doing that forces job changes that means massive career damage.

Why should I have to gamble at the same blackjack table as Gordon Gecko? Why can't i just get the 5.25% passbook rate and the government keeps the currency from inflating more than 2% a year per the 1980 method of calculation?

I really think people who play and fuel the markets are either psychopaths or people without kids. And these people are gambling away the foundation for the next generation.

Its the era of the oligarchs and the 0.01%. The middle class is basically done, and the middle class doesnt become the 1% or the upper middle class at DOW 50000, because that will mean $10 gas and pizza delivery at $50+ a large pie. our standard of living is in drastic decline and the salaries are stagflating and most companies dont have as generous ESPP, RSUs and 401k match as they used to. Sometimes non at all. And pensions and/or defined benefit plans? Hah! Gone.

So we all must gamble at the steps of FedZilla, putting our lives and our kids future on the table.

This isnt going to end well.

Today the DOW is up over 13,000 for the first time since 2008

As priced in dollars. The dollar is worth less now than it was in 2008.

Sometimes I think the only real hope for a USA manufacturing boom, would be if we sell our weapons and rent our military indiscriminately to any and every last nutjob with cash and a grudge.

True! Ever see the movie "Canadian Bacon"?

edvard2, my goal here is to understand what's going on and to analyze the magnitude of the risk.

Good thoughts.

For example, guns and gold for doomsday believers. If you think bad inflation is coming, stocks are actually a good choice as we say hello to Dow 50,000. If you think deflation for now but things will recover without default or bad inflation, then government bonds are a great deal.

It's not a black and white picture in the inflation vs. deflation debate, it's more like both are going on at the same time in different assets.

You'd just want to be adequately hedged in any scenario.

And just FYI, Hyperinflation is not really bad inflation, it's the after-effect of a severe deflation.

What I am saying though is that credit deflation is pretty much guaranteed (my original post), nevertheless the outcome of this credit deflation is in the whimsical hands of monetary policy and fiscal policy makers.

In fact, we don't exactly know how this debacle will unfold, so claiming one solution over another is like betting blindly. The only thing we know is that someone's gonna get hurt... real bad!

True.

The one-dimensional thought process (stocks are always good) is yet another symptom of normalcy bias.

In fact the market has been doing pretty well for some time now. So is it better to sit around and worry about what might or might not happen?

Stability does not equal resilience.

In fact macro economic stabilization causes the macro economy to be even more fragile.

See this for more: http://www.macroresilience.com/2010/10/18/the-resilience-stability-tradeoff-drawing-analogies-between-river-management-and-macroeconomic-management/

I just saw in the WSJ a couple of days ago that Catepillar insourced over 1,000 jobs from Japan to Georgia. I know there's a lot of moving parts, but we're still trying to recover from the massive misallocation of resouces (people involved in construction, finance, and ancilliary RE services) from the housing bubble.

Guess its worth repeating and even though is tiresome and well-worn it applies to this topic as well:

For the past 100+ years the stock market has performed on average of 7-10% annual gains over the long term- as in if you invested 20-40 years ago you would be considerably more well-off than when you started even if you contributed nothing between then and now. Most people for some reason simply don't trust these numbers.

Are the baaaaad ole' days around the corner? Who knows? The same question was asked probably back in 1880, 1881, 1882, 1883....... and so on. Bad times are always possibly right around the corner. There were definitely a huge number of problems back then as there is now. There always has been. We can sit here and analyze all day long and talk doom and gloom till' the cows come home. Likewise we could do nothing but spurt happy flowers out of our noses and talk about oh-how-wonderful things are and always will be. Neither approach is accurate, beneficial, nor does it help to solve the ultimate question which is how to possibly forever mitigate risk and assure smooth sailing. Why? Because no such solution exists.

But let's say that some of you are right and that "Things are different this time". What's going to happen? Are the smartest people going to be the ones who cleverly dug caves and stocked them full of canned beans? I could go on but the point being made is that even if the most cautious,most well-prepared person were to somehow make their lives revolve around preparing for the inevitable worse-case economic scenario then what would guarantee that they made the right preparations? They- just like the boring ole' guy who stuck money into a 401k made a guess and in turn are making a risk-based decision based on what they believe to be true. They're no different than anyone else at the end of the day.

Thus again the only thing left is historical averaging and statistics. Thus why I- as a very cautious, conservative and utterly pessimistic investor simply invest in the overall broad market. That isn't to say that suddenly the stock market could for some unforeseen reason collapse. That's always been and always will be a risk. But given its past performance I put my trust into it more so than other investments.

*Not financial advice.

For the past 100+ years the stock market has performed on average of 7-10% annual gains over the long term- as in if you invested 20-40 years ago you would be considerably more well-off than when you started even if you contributed nothing between then and now. Most people for some reason simply don't trust these numbers.

Had to many friends get hurt as retail investors. I had family lose hundreds of THOUSANDS at various times not just the nineties. Thing is like Vegas you never hear about the losses cause folks feel shame. It usually comes out in the wash over a couple of beers.

You are a true believer. I hope you time it right.

what would guarantee that they made the right preparations?

No guarantees. But just because there are "no guarantees" doesn't mean that one shouldn't prepare.

Most people for some reason simply don't trust these numbers.

Markets can be depressed (in terms of real value) for very long periods of time. Yes, it's great over the long run, but if SHTF today, are you prepared not to get your money's worth for up to 2 decades? Perhaps it's best to hedge.

Either way, good luck. If things don't go so well, please don't blame any of us here on patrick.net.

Had to many friends get hurt as retail investors.

And during the dot com bust, people flock to real estate.

Hyperinflation is not really bad inflation, it's the after-effect of a severe deflation.

I've been avoiding the term, simply because I haven't drawn the lines between bad inflation and hyperinflation (not mentioning the cause).

For instance, the Mexican peso inflated 1000-to-1 in the 90's. Then they began issuing the new Mexican peso, which is equal to 1000 of the old. I would categorize that as hyperinflation. What about a 4-to-1 or even a 2-to-1 inflation?

Also, both Weimar and Zimbabwe were all cash environments with outright refusal to stop printing money in exponentially growing quantities. I blame Havenstein and Mugabe. The Mexican peso stopped at 1000x. So I don't really believe in runaway hyperinflation in that sense.

Do people "lose" money in the market? Sure. But most times those people are the ones who panic and pull all their money when the market hits bottom. TONS of people did that this time around and they definitely lost money... because they pulled out. Had they left their money in place, they- like me, would already be back up to where they were before the crash and likely be gaining. I know because I stuck a lot of money in 2007- right before the bust. My total values went down almost 50%. Now its gaining value over what it was in 2007 and some investments are now gaining double digits.

Let me put this in another way: I know WAY more people who bought houses and lost considerably more money and in many cases defaulted as a result than those I know who lost money in stocks. I also know a considerable amount of ordinary everyday people who had ordinary jobs, didn't buy investment houses, or any other investment and are now basically millionaires because all they ever did was invest in their little 401k's and mutual funds.

This isn't an all or nothing decision. Truth be known it takes a shockingly small amount of money to invest in the market in order to do well. The old saying goes that in general a person should invest 10% of their income into retirement funds. So its not like those paying into retirement funds are breaking their banks doing so.

Then again, most American don't know this. If they did more people would be set fire retirement. I don't have to be a believer. I look at historical facts and trends.

- Not investment advice

Do people "lose" money in the market? Sure. But most times those people are the ones who panic and pull all their money when the market hits bottom. TONS of people did that this time around and they definitely lost money...

No bunny quotes Ed. My folks lost a ton. Some things never came back and they were already ready to retire. Not investment advice either just something to think on

No bunny quotes Ed. My folks lost a ton. Some things never came back and they were already ready to retire. Not investment advice either just something to think on

Well, that would be the case for anyone about to retire no matter what they had invested in. I can guarantee that there were TONS of folks who were just about ready to retire here in the Bay Area, who owned homes and due to their cost were counting on them as their "retirement". Then the bust hit and bingo- they lost their retirement.

Any investment requires planning. When you're younger and have time, that is when you should stomach more risk. When you get older that's the time to pull back and invest in less risky things.

Right now I am in my early 30's and have a ton of time to let the market work.

-not investment advice

Are the smartest people going to be the ones who cleverly dug caves and stocked them full of canned beans? I could go on but the point being made is that even if the most cautious,most well-prepared person were to somehow make their lives revolve around preparing for the inevitable worse-case economic scenario then what would guarantee that they made the right preparations?

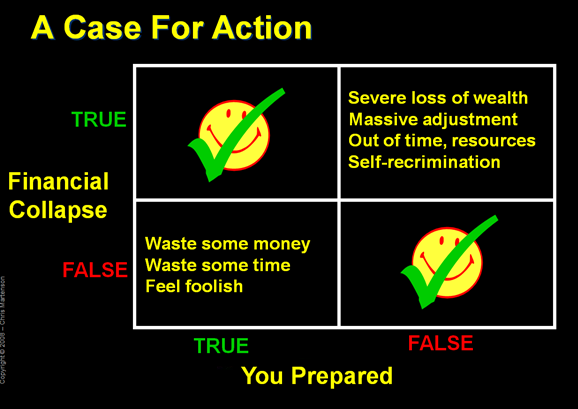

Edvard,

check out this slide (borrowed from Chris Martenson's Crash course)

Edvard,

check out this slide (borrowed from Chris Martenson's Crash course)

I fail to see anything that really changes facts. Sorry. Either way- if some people think the economy is on the verge on collapse and don't feel comfortable investing.... Then DON'T. Simple as that. But that same advice goes for those investing in ANYTHING. Doesn't matter what 'thing' a person invests in. ALL of it is under the same risk factors. There is absolutely zero difference.They aren't any safer financially than anyone else. So that being the case, what exactly is being argued here? That someday there will be an economic collapse? Well- in my opinion "someday" my car could break down on the freeway. One day I could win the lotto. One day we could run out of helium. One day all the bees could die of a bee virus and we'd be reduced to eating corn-based mush. So either we can all sit around biting out fingernails and worry about each and every possible disastrous outcome or we could simply enjoy things as they are at the present.

Let me finalize that I too was VERY much one of those chicken little, persistently pessimistic, doom and gloom, the economy is gonna' collapse folks for years and years. But in the end what good does that do? Well for starters it doesn't make any money. So until that possible collapse comes I'll keep right on making some money. Nuttin' wrong with that... right?

- not financial advice

For the past 100+ years the stock market has performed on average of 7-10% annual gains over the long term-

Flat Decades:

1929-1954

1967-1982

2000-2012+

If you invested money at age 40 in these markets, and held for the 12+ years, you made bupkiss, while incurring an opportunity cost with your stagnant money.

Say you turned 35 in 2000 and put $15,000 in the market. Is it worth it to keep your money in the stock market, at a loss for going on 12 years, or should you have spent it on an small old sailboat and taught your kids to sail in the bay? Plus, you can still sell the now ancient boat for a few thousand bucks and recoup some of the costs after you enjoyed it.

Last comment because obviously this is a non-ending circular argument and everyone already made up their mind thus there's no use repeating the same crap over and over again. I HAVE made money in the stock market and continue to do so. It basically paid for my college education and my first truck. What's more is that after all the badness of the recession we're in had peaked I am making money once more. Most people panicked and pulled out. I didn't. In fact some of my relatives are the ones who are now basically sitting pretty because they invested consistently all along and did nothing but stick money into 401k's and did so all throughout their lives and that includes a lot of those "flat" decades. Its so simple and easy, which is perhaps why most people simply don't get it. Time and my experience along with the experiences of those I know who consistently invest has more or less proven that the market works if you are patient.

Either way, good luck to the rest of you guys. Over and out.

- Not investment advice.

I don't think patience is the equalizer. I think it's more like luck. For every one retail investor who gets lucky in the stock market dozens of others are eviscerated. I know them. I have personal pals who scrimped and pinched they whole lives and had towels on their couches for slip covers and didn't run the air in the cars in 118 degree heat and counted out each piece of rice they would eat before cooking it up, all because they funnelled as much dough into the stock market as they could. They all either ended up flat or busted, living in their in-laws basement or something. It made me get what little I had in there the hell out. I bought a Tutti Fruitti which has been doing great and also brings smiles to the faces of children and adults alike with our wonderful montage of fruit flavors.

By the way, it is not always totally clear what the safe bets are. It's really not unlike Vegas in that way.

Also not investment advice.

Truth be told, nobody gets rich from index funds. They're probably better than bank accounts.

Real wealth comes from starting businesses (or investing when they're small), landing an obscenely well paying job (CEO, professional athlete), or doing something illegal.

Truth be told, nobody gets rich from index funds. They're probably better than bank accounts.

Real wealth comes from starting businesses (or investing when they're small), landing an obscenely well paying job (CEO, professional athlete), or doing something illegal.

Real wealth comes from starting businesses (or investing when they're small), landing an obscenely well paying job (CEO, professional athlete), or doing something illegal.

According to my observations many CEOs don't get rich from their job payments, but from "investing", while being in positions to influence market valuations. (or, well you've covered this under "doing something illegal")

The more unethical the person, the easier it is for them to make lots of money.

If you had any doubt:

Friedman even said Fisher was the greatest American economist, and I think that is correct. Fisher had a broader understanding of the economy in a very, very critical way and in a way that I don’t think either Friedman or John Maynard Keynes understood it, and even a lot of contemporary economists, such as Ben Bernanke. Keynes and Friedman both felt that The Great Depression was due to an insufficiency of aggregate demand and so the way you contained a Great Depression was by your response to the insufficiency of aggregate demand. For Keynes, that was by having the federal government borrow more money and spend it when the private sector wouldn’t. And for Friedman, that was for the Federal Reserve to do more to stimulate the money supply so that the private sector would lend more money. Fisher, on the other hand, is saying something entirely different. He’s saying that the insufficiency of aggregate demand is a symptom of excessive indebtedness and what you have to do to contain a major debt depression event — such as the aftermath of 1873, the aftermath of 1929, the aftermath of 2008 — is you have to prevent it ahead of time. You have to prevent the buildup of debt.

Full Link