patrick.net

An Antidote to Corporate Media

1,191,902 comments by 13,863 users - AmericanKulak, ForcedTQ, Patrick, The_Deplorable online now

I'm liquidating my stocks and going to cash

2019 Mar 28, 10:56am 4,944 views 73 comments

Comments 1 - 40 of 73 Next » Last » Search these comments

1

anonymous

2019 Mar 28, 11:00am

Interesting thread title - that was used about three years ago, maybe a bit less from the commenter from Lafayette, CA.

Sounds like a very timely move right now.

Sounds like a very timely move right now.

2

Shaman

2019 Mar 28, 11:04am

Shaman

2019 Mar 28, 11:04am

Kakistocracy says

Pretty awful move, if he actually did it. My prediction from that time was far more accurate.

http://patrick.net/post/1300205/2016-12-14-the-coming-economic-boom

Interesting thread title - that was used about three years ago, maybe a bit less from the commenter from Lafayette, CA.

Pretty awful move, if he actually did it. My prediction from that time was far more accurate.

http://patrick.net/post/1300205/2016-12-14-the-coming-economic-boom

3

Heraclitusstudent

2019 Mar 28, 11:07am

Iwog was early and I might be too.

"There is a tide in the affairs of men.

Which, taken at the flood, leads on to fortune;

Omitted, all the voyage of their life

Is bound in shallows and in miseries.

On such a full sea are we now afloat,

And we must take the current when it serves,

Or lose our ventures."

"There is a tide in the affairs of men.

Which, taken at the flood, leads on to fortune;

Omitted, all the voyage of their life

Is bound in shallows and in miseries.

On such a full sea are we now afloat,

And we must take the current when it serves,

Or lose our ventures."

4

Shaman

2019 Mar 28, 11:11am

Heraclitusstudent says

Of course you’re correct that such things are cyclical. And that timing is everything.

I missed the real estate bottom by a couple years because I was thinking pure economics. That particular person actually set me straight just in time to make some money in the market.

Iwog was early and I might be too.

Of course you’re correct that such things are cyclical. And that timing is everything.

I missed the real estate bottom by a couple years because I was thinking pure economics. That particular person actually set me straight just in time to make some money in the market.

5

anonymous

2019 Mar 28, 11:14am

Heraclitusstudent - better to leave a bit on the table and walk away with a decent take then let greed take over and risk losing more than you bargained for.

7

Rin

2019 Mar 28, 11:35am

Rin

2019 Mar 28, 11:35am

Liquidate all stocks which are cap gain plays only.

Otherwise, hold onto those DRIPs (& no, not GE or Heinz) because that 4% dividend will spike to 8-10%, which will nearly double one's equity holdings during the downturn.

Otherwise, hold onto those DRIPs (& no, not GE or Heinz) because that 4% dividend will spike to 8-10%, which will nearly double one's equity holdings during the downturn.

8

CBOEtrader

2019 Mar 28, 11:40am

CBOEtrader

2019 Mar 28, 11:40am

Heraclitusstudent says

Agree w your risk assessment. Cash though? Are you even doing a 1 year CD or fricken crypto bets or anything? Just straight cash?

Rash... I know.

Agree w your risk assessment. Cash though? Are you even doing a 1 year CD or fricken crypto bets or anything? Just straight cash?

9

Heraclitusstudent

2019 Mar 28, 11:41am

Rin says

Am I not better off holding some kind of long bond returning 3% and then reinvest progressively to stocks for example when I see weekly unemployment claims spike?

I understand you eliminate timing. But there are recognizable patterns in the way these things unfold.

Otherwise, hold onto those DRIPs (& no, not GE or Heinz) because that 4% dividend will spike to 8-10%, which will nearly double one's equity holdings during the downturn.

Am I not better off holding some kind of long bond returning 3% and then reinvest progressively to stocks for example when I see weekly unemployment claims spike?

I understand you eliminate timing. But there are recognizable patterns in the way these things unfold.

10

EBGuy

2019 Mar 28, 11:41am

Speaking of Ducky, if I remember correctly, he made small fortune last time around by literally hauling around a wheel barrow full of silver. The gold/silver ratio is above 85 and has been consistently above 80 the last half a year. One of them has gotta give soon (either gold collapses or silver rises). I've been contemplating moving some retirement cash into SLV as a hedge.

11

CBOEtrader

2019 Mar 28, 11:48am

Quigley says

Liquidating into the volatile election not the worst idea, but he should have bought back in a month later. In fact, I'd bet IWOG bought back in at some point. Hes smart enough to identify a trend.

To the OP point, the recent extra volatility is a signal for increased chances of a market downturn.

This is exactly what my research suggests as well. Watch the vix. The relevant resistance points are 18, 22, 28, and 35. Above each, we go into a new distinctly more challenging market environment...and YES the vix itself is both a signal for increased bearish pressure and OVERPERFORMANCE of implied vol. (Or underperformance at low IV's.)

Ex: Sell options when vix is below 22. Do nothing from vix 22 to 28, and buy puts when vix is > 28.

^^ this by itself is a winning trading strategy.

Heraclitusstudent saysIwog was early and I might be too.

Of course you’re correct that such things are cyclical. And that timing is everything.

I missed the real estate bottom by a couple years because I was thinking pure economics. That particular person actually set me straight just in time to make some money in the market.

Liquidating into the volatile election not the worst idea, but he should have bought back in a month later. In fact, I'd bet IWOG bought back in at some point. Hes smart enough to identify a trend.

To the OP point, the recent extra volatility is a signal for increased chances of a market downturn.

This is exactly what my research suggests as well. Watch the vix. The relevant resistance points are 18, 22, 28, and 35. Above each, we go into a new distinctly more challenging market environment...and YES the vix itself is both a signal for increased bearish pressure and OVERPERFORMANCE of implied vol. (Or underperformance at low IV's.)

Ex: Sell options when vix is below 22. Do nothing from vix 22 to 28, and buy puts when vix is > 28.

^^ this by itself is a winning trading strategy.

12

Heraclitusstudent

2019 Mar 28, 12:44pm

CBOEtrader says

Long treasuries and tax free municipal. Waiting for yields to bounce back a bit.

Just straight cash?

Long treasuries and tax free municipal. Waiting for yields to bounce back a bit.

13

BayArea

2019 Mar 28, 12:51pm

BayArea

2019 Mar 28, 12:51pm

You might be right

Or you might be wrong and miss out on 15% gain this year lol

Or you might be wrong and miss out on 15% gain this year lol

14

CBOEtrader

2019 Mar 28, 2:14pm

Heraclitusstudent says

Careful there homie. Treasuries fall in value as rates rise. Considering the flat to inverted yield curve, just keep it super short

CBOEtrader saysJust straight cash?

Long treasuries and tax free municipal. Waiting for yields to bounce back a bit.

Careful there homie. Treasuries fall in value as rates rise. Considering the flat to inverted yield curve, just keep it super short

15

CBOEtrader

2019 Mar 28, 2:14pm

BayArea says

he's trying to dodge a possible 40% correction, but you are correct

You might be right

Or you might be wrong and miss out on 15% gain this year lol

he's trying to dodge a possible 40% correction, but you are correct

17

Heraclitusstudent

2019 Mar 28, 3:03pm

CBOEtrader says

As long as we have a revenue shortfall financed by debt, we are solidly anchored on the deflationary side of things.

I see the rates risk as minimal for now.

Careful there homie. Treasuries fall in value as rates rise.

As long as we have a revenue shortfall financed by debt, we are solidly anchored on the deflationary side of things.

I see the rates risk as minimal for now.

18

Heraclitusstudent

2019 Mar 28, 3:29pm

10yr treasury rate will probably fall to low 1% in case of recession.

19

EBGuy

2019 Mar 28, 3:36pm

0ba4 says

Not just bondz. CA TAX-FREE MUNI Bond FUNDZ! WITH LEVERAGE! Who can forget NAC? How soon they forget.

In all fairness, I believe he used NAC in the trusts he managed for generating cash.

When the Duck said cash, it meant bonds

Not just bondz. CA TAX-FREE MUNI Bond FUNDZ! WITH LEVERAGE! Who can forget NAC? How soon they forget.

In all fairness, I believe he used NAC in the trusts he managed for generating cash.

20

Heraclitusstudent

2019 Mar 28, 3:48pm

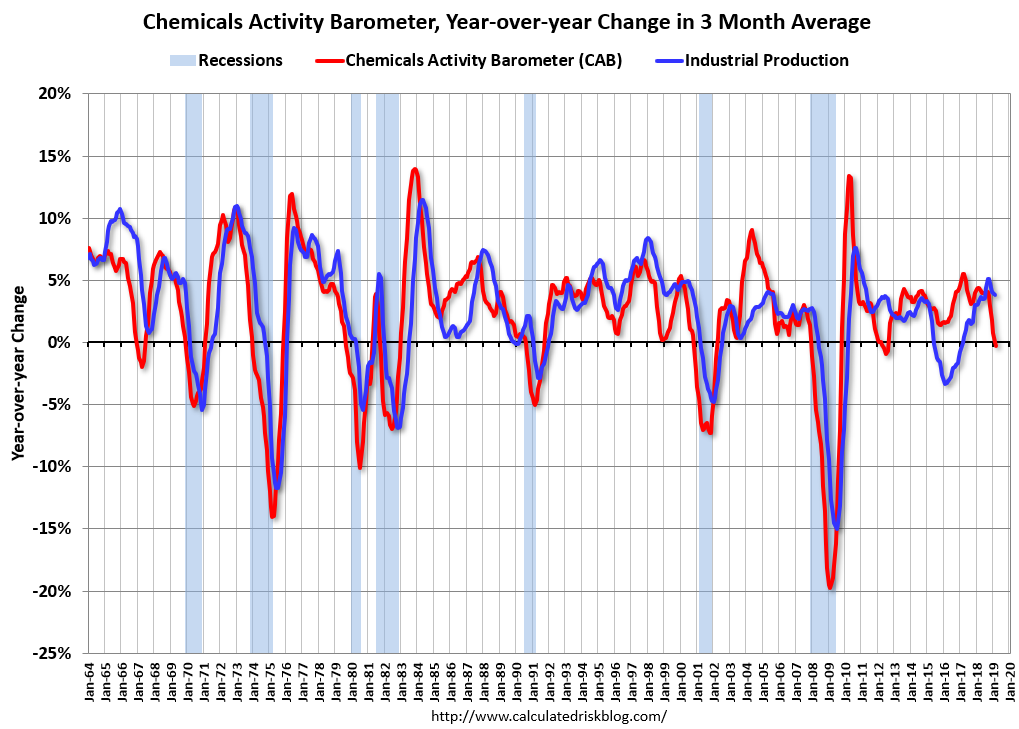

Appendix A: In 7 out of 9 past times this indicator fell to 0, recession ensued.

21

CBOEtrader

2019 Mar 28, 4:06pm

EBGuy says

talk about playing w fire, wow

0ba4 saysWhen the Duck said cash, it meant bonds

Not just bondz. CA TAX-FREE MUNI Bond FUNDZ! WITH LEVERAGE! Who can forget NAC? How soon they forget.

In all fairness, I believe he used NAC in the trusts he managed for generating cash.

talk about playing w fire, wow

22

CBOEtrader

2019 Mar 28, 4:07pm

Heraclitusstudent says

interesting chart

Appendix A: In 7 out of 9 past times this indicator fell to 0, recession ensued.

interesting chart

23

CBOEtrader

2019 Mar 28, 4:11pm

Heraclitusstudent says

I'd worry about not having a recession if you are long the 10 year bonds. Fact is indicators are starting to point down, which can easily reverse. This could very likely (even probably) be a headfake. SO, you are risking missing out the bull market AND eating some losses in your bonds IF the market indicators reverse.

I'm not saying its the wrong move. I am saying your position is not inherently less risky than being long the stock market

10yr treasury rate will probably fall to low 1% in case of recession.

I'd worry about not having a recession if you are long the 10 year bonds. Fact is indicators are starting to point down, which can easily reverse. This could very likely (even probably) be a headfake. SO, you are risking missing out the bull market AND eating some losses in your bonds IF the market indicators reverse.

I'm not saying its the wrong move. I am saying your position is not inherently less risky than being long the stock market

24

mell

2019 Mar 28, 4:25pm

I don't think there will be a recession before 2020 or 2021. The economy is too strong. Sure the fat days of appreciation are over and it will be more volatile which is nice for active traders but I don't see any crash or recession.

25

mell

2019 Mar 28, 4:26pm

But one or two years early is not the worst thing. Or trade biotech mostly event driven and relatively recession proof. But also extremely risky.

26

Heraclitusstudent

2019 Mar 28, 4:31pm

You are right, there is a risk. But remember: no one is paid not to take risks.

Overstaying the rally is a real risk too that becomes larger as the market climbs.

Even if there is a bounce back, it will likely not be for too long until the recession actually comes. So I lose a bit of upside: I say it becomes picking up pennies in front of the steamroller.

There just comes a time when you need to roll your dice.

Iwog did it. Turns out too early.

I do it now. We'll see.

Overstaying the rally is a real risk too that becomes larger as the market climbs.

Even if there is a bounce back, it will likely not be for too long until the recession actually comes. So I lose a bit of upside: I say it becomes picking up pennies in front of the steamroller.

There just comes a time when you need to roll your dice.

Iwog did it. Turns out too early.

I do it now. We'll see.

27

mell

2019 Mar 28, 4:35pm

Heraclitusstudent says

I definitely think faang and tech in general has seen their highs.

You are right, there is a risk. But remember: no one is paid not to take risks.

Overstaying the rally is a real risk too that becomes larger as the market climbs.

Even if there is a bounce back, it will likely not be for too long until the recession actually comes. So I lose a bit of upside: I say it becomes picking up pennies in front of the steamroller.

There just comes a time when you need to roll your dice.

Iwog did it. Turns out too early.

I do it now. We'll see.

I definitely think faang and tech in general has seen their highs.

28

mell

2019 Mar 28, 4:38pm

That being said I think we will see DOW 30K. Keep in mind a lot of the economic news are spun negatively due to TDS. If this were a leftoid presidency the media would ring in a new economic golden age.

30

EBGuy

2019 Mar 28, 4:41pm

CBOEtrader says

Man cannot live on treasuries alone. It was yielding 6+% (Tax free) five years ago -- income's gotta come from somewhere. YMMV. NAC is currently yielding 4.8%.

talk about playing w fire, wow

Man cannot live on treasuries alone. It was yielding 6+% (Tax free) five years ago -- income's gotta come from somewhere. YMMV. NAC is currently yielding 4.8%.

31

mell

2019 Mar 28, 4:47pm

APOCALYPSEFUCKisShostikovitch says

What happened to the promised real estate carnage? I'm ready

CASH! is wonderful but by the end, the only currency anyone will care about will be belt-fed ammo and YAM!s.

What happened to the promised real estate carnage? I'm ready

32

Heraclitusstudent

2019 Mar 28, 4:52pm

The understated engine of this cycle has been the recovery of housing, driving a stock market obsessed with tech. Housing prices are now slowing. That fuel is spent.

Trees do not grow to the sky.

Trees do not grow to the sky.

33

mell

2019 Mar 28, 4:54pm

Heraclitusstudent says

I agree but it's mostly housing and a couple of tech trannies that are massively overvalued. The P/E for most stocks is still absolutely reasonable.

The understated engine of this cycle has been the recovery of housing, driving a stock market obsessed with tech. Housing prices are now slowing. That fuel is spent.

Trees do not grow to the sky.

I agree but it's mostly housing and a couple of tech trannies that are massively overvalued. The P/E for most stocks is still absolutely reasonable.

36

EBGuy

2019 Mar 28, 5:21pm

Heraclitusstudent says

I don't disagree, but most of the refund checks haven't been sent out yet. Plenty of non-coastal folks will be getting money back. More sugar to get us through the next election cycle. At this point, though, the tax code is loaded with buried IEDs. Almost unfixable as the Dems (or responsible adults in Congress) will have to argue for tax increases at the same time that they advocate for tax cuts (dispensing with SALT limits) for the coastal elites. This situation is nearly unfixable, so when the house of cards comes down it will blow out spectacularly.

Trump's tax cut is spent too. Sugar high.

I don't disagree, but most of the refund checks haven't been sent out yet. Plenty of non-coastal folks will be getting money back. More sugar to get us through the next election cycle. At this point, though, the tax code is loaded with buried IEDs. Almost unfixable as the Dems (or responsible adults in Congress) will have to argue for tax increases at the same time that they advocate for tax cuts (dispensing with SALT limits) for the coastal elites. This situation is nearly unfixable, so when the house of cards comes down it will blow out spectacularly.

37

Heraclitusstudent

2019 Mar 28, 5:27pm

I dislike "technical analysis" but this is one chart is fucking ugly:

38

CBOEtrader

2019 Mar 28, 7:03pm

EBGuy says

Are you calling for a dollar crash? Are you loaded up on mortgages?

Perhaps an XRP play if you really think the global exchange system could collapse

This situation is nearly unfixable, so when the house of cards comes down it will blow out spectacularly.

Are you calling for a dollar crash? Are you loaded up on mortgages?

Perhaps an XRP play if you really think the global exchange system could collapse

39

Shaman

2019 Mar 28, 7:23pm

Heraclitusstudent says

To me this looks like a trailing indicator. By January 2009, the stock markets had reached close to their low points after falling all 2008. The nadir is after January. So honestly, this would be shit for predictive value. Looking back, the 2001 nadir wasn’t predictive either.

If anything, the bottom on this graph would indicate that there’s six months until the recovery.

Appendix A: In 7 out of 9 past times this indicator fell to 0, recession ensued.

To me this looks like a trailing indicator. By January 2009, the stock markets had reached close to their low points after falling all 2008. The nadir is after January. So honestly, this would be shit for predictive value. Looking back, the 2001 nadir wasn’t predictive either.

If anything, the bottom on this graph would indicate that there’s six months until the recovery.

40

AD

2019 Mar 28, 8:36pm

AD

2019 Mar 28, 8:36pm

Heraclitusstudent says

Yes, basically the S&P 500 has moved sideways for the last 14 months. Notice the S&P 500 moved sideways for about 12 months prior to the late 2008 crash.

Seems like not much left to keep the market propped up around 2800 points for S&P 500. And technically the market was in a bear market back on December 24 when the S&P 500 was down 20% from its recent peak, as well as the other major indices below 20% of their recent peaks.

I dislike "technical analysis" but this is one chart is fucking ugly:

Yes, basically the S&P 500 has moved sideways for the last 14 months. Notice the S&P 500 moved sideways for about 12 months prior to the late 2008 crash.

Seems like not much left to keep the market propped up around 2800 points for S&P 500. And technically the market was in a bear market back on December 24 when the S&P 500 was down 20% from its recent peak, as well as the other major indices below 20% of their recent peaks.

Comments 1 - 40 of 73 Next » Last » Search these comments

I think the best we can hope at this point is 1 year of slow growth and a volatile market before some kind of recession.